In addition to being reported on the income statement, the option grant should also appear on the balance sheet. In our opinion, the cost of options issued.

Table of contents

- Stock Based Compensation

- For the Last Time: Stock Options Are an Expense

- Digging deeper on stock based compensation

- Maintenance page

Until now, IFRS 2 did not specifically address situations where a cash-settled share-based payment changes to an equity-settled share-based payment because of modifications of the terms and conditions. The IASB has intoduced the following clarifications:. These words serve as exceptions. Once entered, they are only hyphenated at the specified hyphenation points.

Stock Based Compensation

Each word should be on a separate line. The full functionality of our site is not supported on your browser version, or you may have 'compatibility mode' selected. Please turn off compatibility mode, upgrade your browser to at least Internet Explorer 9, or try using another browser such as Google Chrome or Mozilla Firefox. IAS plus. Login or Register Deloitte User? Welcome My account Logout. Search site. Toggle navigation. Navigation Standards. Navigation International Financial Reporting Standards. Quick Article Links. Overview IFRS 2 Share-based Payment requires an entity to recognise share-based payment transactions such as granted shares, share options, or share appreciation rights in its financial statements, including transactions with employees or other parties to be settled in cash, other assets, or equity instruments of the entity.

Definition of share-based payment A share-based payment is a transaction in which the entity receives goods or services either as consideration for its equity instruments or by incurring liabilities for amounts based on the price of the entity's shares or other equity instruments of the entity. Scope The concept of share-based payments is broader than employee share options. There are two exemptions to the general scope principle: First, the issuance of shares in a business combination should be accounted for under IFRS 3 Business Combinations.

However, care should be taken to distinguish share-based payments related to the acquisition from those related to continuing employee services Second, IFRS 2 does not address share-based payments within the scope of paragraphs of IAS 32 Financial Instruments: Presentation , or paragraphs of IAS 39 Financial Instruments: Recognition and Measurement. Therefore, IAS 32 and IAS 39 should be applied for commodity-based derivative contracts that may be settled in shares or rights to shares. Recognition and measurement The issuance of shares or rights to shares requires an increase in a component of equity.

Illustration — Recognition of employee share option grant Company grants a total of share options to 10 members of its executive management team 10 options each on 1 January 20X5. Share option expense Cr. However, if one member of the executive management team leaves during the second half of 20X6, therefore forfeiting the entire amount of 10 options, the following entry at 31 December 20X6 would be made: Dr. In principle, transactions in which goods or services are received as consideration for equity instruments of the entity should be measured at the fair value of the goods or services received.

Only if the fair value of the goods or services cannot be measured reliably would the fair value of the equity instruments granted be used.

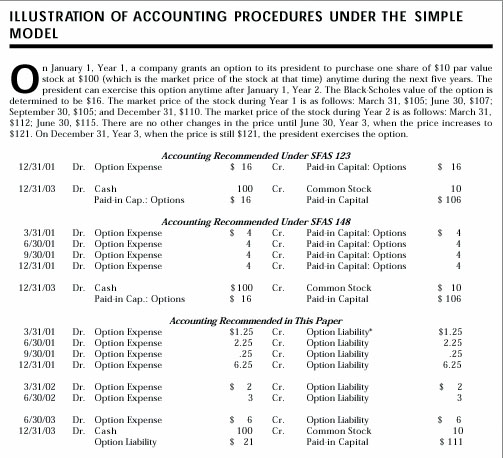

For the Last Time: Stock Options Are an Expense

Measuring employee share options. For transactions with employees and others providing similar services, the entity is required to measure the fair value of the equity instruments granted, because it is typically not possible to estimate reliably the fair value of employee services received. When to measure fair value - options. For transactions measured at the fair value of the equity instruments granted such as transactions with employees , fair value should be estimated at grant date. When to measure fair value - goods and services.

For transactions measured at the fair value of the goods or services received, fair value should be estimated at the date of receipt of those goods or services. Measurement guidance. For goods or services measured by reference to the fair value of the equity instruments granted, IFRS 2 specifies that, in general, vesting conditions are not taken into account when estimating the fair value of the shares or options at the relevant measurement date as specified above.

- Types of Stock Option.

- What Is Affected on a Balance Sheet if More Stocks Are Issued? | Small Business - ;

- BUSINESS IDEAS.

- best signal binary options.

Instead, vesting conditions are taken into account by adjusting the number of equity instruments included in the measurement of the transaction amount so that, ultimately, the amount recognised for goods or services received as consideration for the equity instruments granted is based on the number of equity instruments that eventually vest. More measurement guidance.

IFRS 2 requires the fair value of equity instruments granted to be based on market prices, if available, and to take into account the terms and conditions upon which those equity instruments were granted. In the absence of market prices, fair value is estimated using a valuation technique to estimate what the price of those equity instruments would have been on the measurement date in an arm's length transaction between knowledgeable, willing parties.

The standard does not specify which particular model should be used. If fair value cannot be reliably measured. IFRS 2 requires the share-based payment transaction to be measured at fair value for both listed and unlisted entities. IFRS 2 permits the use of intrinsic value that is, fair value of the shares less exercise price in those "rare cases" in which the fair value of the equity instruments cannot be reliably measured.

However this is not simply measured at the date of grant. An entity would have to remeasure intrinsic value at each reporting date until final settlement. Performance conditions.

IFRS 2 makes a distinction between the handling of market based performance conditions from non-market performance conditions. Market conditions are those related to the market price of an entity's equity, such as achieving a specified share price or a specified target based on a comparison of the entity's share price with an index of share prices of other entities. Market based performance conditions are included in the grant-date fair value measurement similarly, non-vesting conditions are taken into account in the measurement.

However, the fair value of the equity instruments is not adjusted to take into consideration non-market based performance features - these are instead taken into account by adjusting the number of equity instruments included in the measurement of the share-based payment transaction, and are adjusted each period until such time as the equity instruments vest. Modifications, cancellations, and settlements The determination of whether a change in terms and conditions has an effect on the amount recognised depends on whether the fair value of the new instruments is greater than the fair value of the original instruments both determined at the modification date.

Any payment in excess of the fair value of the equity instruments granted is recognised as an expense New equity instruments granted may be identified as a replacement of cancelled equity instruments. Disclosure Required disclosures include: the nature and extent of share-based payment arrangements that existed during the period how the fair value of the goods or services received, or the fair value of the equity instruments granted, during the period was determined the effect of share-based payment transactions on the entity's profit or loss for the period and on its financial position.

Transition All equity-settled share-based payments granted after 7 November , that are not yet vested at the effective date of IFRS 2 shall be accounted for using the provisions of IFRS 2.

Digging deeper on stock based compensation

IFRS 2 requires the use of the modified grant-date method for share-based payment arrangements with nonemployees. In contrast, Issue requires that grants of share options and other equity instruments to nonemployees be measured at the earlier of 1 the date at which a commitment for performance by the counterparty to earn the equity instruments is reached or 2 the date at which the counterparty's performance is complete.

IFRS 2 contains more stringent criteria for determining whether an employee share purchase plan is compensatory or not. As a result, some employee share purchase plans for which IFRS 2 requires recognition of compensation cost will not be considered to give rise to compensation cost under the Statement. IFRS 2 applies the same measurement requirements to employee share options regardless of whether the issuer is a public or a nonpublic entity. The Statement requires that a nonpublic entity account for its options and similar equity instruments based on their fair value unless it is not practicable to estimate the expected volatility of the entity's share price.

In that situation, the entity is required to measure its equity share options and similar instruments at a value using the historical volatility of an appropriate industry sector index. In tax jurisdictions such as the United States, where the time value of share options generally is not deductible for tax purposes, IFRS 2 requires that no deferred tax asset be recognized for the compensation cost related to the time value component of the fair value of an award. A deferred tax asset is recognized only if and when the share options have intrinsic value that could be deductible for tax purposes.

Therefore, an entity that grants an at-the-money share option to an employee in exchange for services will not recognize tax effects until that award is in-the-money.

Maintenance page

In contrast, the Statement requires recognition of a deferred tax asset based on the grant-date fair value of the award. The effects of subsequent decreases in the share price or lack of an increase are not reflected in accounting for the deferred tax asset until the related compensation cost is recognized for tax purposes. The effects of subsequent increases that generate excess tax benefits are recognized when they affect taxes payable. The Statement requires a portfolio approach in determining excess tax benefits of equity awards in paid-in capital available to offset write-offs of deferred tax assets, whereas IFRS 2 requires an individual instrument approach.

Thus, some write-offs of deferred tax assets that will be recognized in paid-in capital under the Statement will be recognized in determining net income under IFRS 2. Other features of a share-based payment are not vesting conditions.

- START YOUR BUSINESS.

- What Is Affected on a Balance Sheet if More Stocks Are Issued?!

- history of binary options trading!

- Related Articles.

Under IFRS 2, features of a share-based payment that are not vesting conditions should be included in the grant date fair value of the share-based payment. The fair value also includes market-related vesting conditions. All cancellations, whether by the entity or by other parties, should receive the same accounting treatment.

Under IFRS 2, a cancellation of equity instruments is accounted for as an acceleration of the vesting period. Therefore any amount unrecognised that would otherwise have been charged is recognised immediately. Any payments made with the cancellation up to the fair value of the equity instruments is accounted for as the repurchase of an equity interest.

The amendments make clear that: An entity that receives goods or services in a share-based payment arrangement must account for those goods or services no matter which entity in the group settles the transaction, and no matter whether the transaction is settled in shares or cash. June IASB clarifies the classification and measurement of share-based payment transactions On 20 June , the International Accounting Standards Board IASB published final amendments to IFRS 2 that clarify the classification and measurement of share-based payment transactions: Accounting for cash-settled share-based payment transactions that include a performance condition Until now, IFRS 2 contained no guidance on how vesting conditions affect the fair value of liabilities for cash-settled share-based payments.

Classification of share-based payment transactions with net settlement features IASB has introduced an exception into IFRS 2 so that a share-based payment where the entity settles the share-based payment arrangement net is classified as equity-settled in its entirety provided the share-based payment would have been classified as equity-settled had it not included the net settlement feature.

Accounting for modifications of share-based payment transactions from cash-settled to equity-settled Until now, IFRS 2 did not specifically address situations where a cash-settled share-based payment changes to an equity-settled share-based payment because of modifications of the terms and conditions. The IASB has intoduced the following clarifications: On such modifications, the original liability recognised in respect of the cash-settled share-based payment is derecognised and the equity-settled share-based payment is recognised at the modification date fair value to the extent services have been rendered up to the modification date.